What are the Treasury Bills in India? – Maturity Period | Features | Issued by

What are the Treasury Bills in India?

In this article, we will discuss “What are the Treasury Bills in India?“.

Anyway, before getting into the start this article, Let me tell you “What is the Government Security?“.

A Government Security also called as G-Sec, is a tradeable instrument issued by the Central or the State Governments.

It acknowledges the Government’s debt obligation.

Such Government securities are short-term, knows as Treasury Bills or T-bills, with original maturities of less than one year.

In other side, original maturity of one year or more than knows as Government Bonds or Dated Securities.

The Central Government issues both, T-Bills and Bonds while the State Governments issue only bonds, which are known as State Development Loans (SDLs).

Let’s understand treasury bills with easy way, the Central Government also needs funds to build infrastructure, hospitals, etc. When they run short of fund, they approach their bank for a mortgage, which is the RBI.

The Reserve Bank of India, in turn, auctions the mortgage in the form of bonds or treasury bills that you can buy.

Actually, you are lending a part of the overall mortgage the government is seeking.

Against this mortgage, the Central Government, guarantees to pay periodic interest and repay the principal at the end of the tenure.

Also Read Sovereign Gold Bond : Best Returns on Gold Investment | 2020-21 Dates

Eligibility

The T-Bills may be held by –

- An individual, not being a Non-Resident Indian

his or her individual capacity, or

Individual capacity on joint basis, or

Individual capacity on any one or survivor basis, or - A Hindu Undivided Family.

- Banks, dealers (primary), mutual funds, financial institutions and insurance organization.

Also Read RBI Bonds 2021 or Floating Rate Savings Bonds | Rate of Interest | Online & Offline

Maturity Period

Maturity period may classify into three they are:

| 91 days | The tenor of these T-bills complete on 91 days. |

| 182 days | These T-bills get matured after 182 days, from the day of issue. |

| 364 days | These T-bills complete their maturity 364 days from the date of issue. |

- T-bills are available for a minimum amount of INR 25,000/- and in multiples of INR 25,000/-.

- The RBI conducts auctions usually every Wednesday to issue Treasury Bills.

However, payments for the T-bills purchased are made on the following Friday. - The RBI issues T-bills calendar for auction. It declares the exact date of the auction,

the funds to be auctioned and the maturity dates before every auction. - Face values & discount rates of T-bills change periodically. However, it’s depending upon the funding needs and policy of monetary, along with total bids placed.

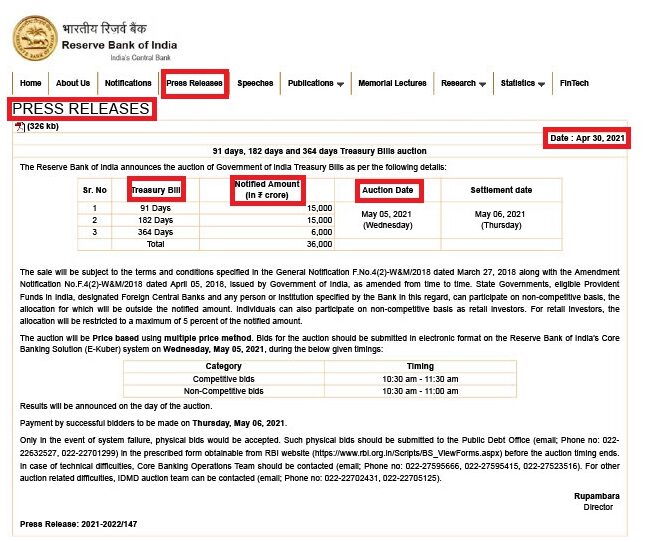

RBI – Press Release for T-Bills

Also Read SBI Capital Gain Bonds | 54EC Bonds | Features | Interest Rate 2021 | How to Buy SBI Online?

Interest Rates for Treasury Bills

As you already know, There are three T-bills types, They are 91 days, 182 days, and 364 days.

T-bills do not carry an interest component. Actually, this is the main difference between T-bills and Bonds.

In other words, these bills are zero coupon securities and pay no interest. Instead, they are issued at a discount and redeemed at the face value at maturity.

These bills are issued at a discount to their PAR i.e. Par value (also called the true value), and upon expiry, it’s redeemed at its true value.

Let’s take an example to understand the calculation of discount value in a better manner.

Also Read NCDs Investment | Upcoming NCDs 2021 | How to Buy? | Risk Factors | NCD vs FD | Best NCDs

Example

For instance, assume the Par Value, is INR 100/-. This T-bill is issued in person at a discount to its PAR, Say INR 96/-. After 91 days, person will get back INR 100/-, and so person makes a return of INR 4/-.

In other word, this is as good as buying a stock at INR 96/- and selling it after 91 days at INR 100/-.

The only difference is that this is a guaranteed transaction, meaning, there is no risk of you selling below INR 100/- (or above INR 100/-).

Considering the same details as above, let us know the exact formula of Treasury Bills rate.

How Do you Calculate Treasury Bill Rate?

The formula is –

Y = (D/P)*(365/N)

Y = Yield

D = Discount Value

P = Bond Price

N = Number of days to maturity

Y = [4/96]*[365/91] = (0.041)*(4.01) =16.7%

Therefore, the treasury bill offers a return on investment of 16.7%. However, since you held it for 91 days, you will enjoy this return on a pro-rata basis.

Logically, 91-day yields are around 6-8%. Needless to say, the higher the yield, the better it is.

Also Read Capital Gain Bonds | Interest Rate | NHAI | REC | PFCL | IRFC | How to Buy Online? |

Bidding Process of Treasury Bills

T-bills are issued in the primary market via auctions conducted by RBI.

An eligible investors, may bid in an auction under Competitive or Non-competitive Bidding facility.

- Competitive Bidding Facility – Institutional investors such as banks, dealers (primary), mutual funds, financial institutions and insurance organization are generally eligible to make competitive bids.

- Non-competitive Bidding Facility – it is open to individuals as a common man, HUFs/trusts, firms, corporate bodies, institutions, provident funds and any other entity.

The noncompetitive Bidding plan will be open to those who-

Do not have CA i.e. current account or SGL i.e. Subsidiary General Ledger account.

Do not require more than INR 1 Cr. (face value) of securities per auction.

A noncompetitive bidder would be able to participate in the auctions of treasury bills without having to quote the yield or price in the bid.

Therefore, bidders will not have to worry about whether his bid will be on or off the mark, as long as he bids in accordance with the plan, the bidder will be allotted securities fully or partially.

Also Read IPOs Definition | Types of IPOs | Fixed Price vs Book Building | Investors Types | Eligibility 2021

Advantages of the Non-Competitive Bidding Facility

- The noncompetitive Bidding facility will encourage wider participation and retail holding of the T-bills.

- This facility enables individuals, firms and other mid segment, investors who do not have the knowledge to bid competitively in the auctions.

- Such investors will have a good chance of assuring allotments at the rate which emerges in the auction.

Features

| Issued by | The Reserve Bank of India |

| Where to buy? | NSE goBid App or Zerodha Kite App or any Demat Account |

| Minimum Bid | INR 25000/- and in the same multiples thereof. |

| Form | These T-bills are issued either in physical form or dematerialized form by a credit to SGL account i.e. subsidiary general ledger. |

| Issue price | T-bills are issued at a discounted price. Although, they are redeemed at par value(PAR) at the time of maturity. |

| Loan facility | NA |

| Risk Factor | Zero Risk |

| Nomination Facility | Yes |

| Transferability | No |

| Tax | T-bills are tax-exempt. However, you will be required to pay a bank fee for the services rendered. |

Key Benefits Of Investment In T-Bills

- No tax deducted at source (TDS).

- Zero default risk being sovereign paper.

- Highly liquid money market instrument.

- Better returns especially in the short term.

- Transparency and simplified settlement.

- High degree of tradeability and active secondary market facilitates meeting unplanned fund requirements.

Also Read Sovereign Gold Bond Calculator : Return Calculation 2021